The online channel accounted for a record 14% of all grocery spend in the UK in the four weeks ending 11 July, according to data from Nielsen. This is up from the 13% share recorded in the previous four weeks, and 10% share in May.

The data shows that online sales over the month surged up 115% compared to the same period last year. Overall total till sales growth slowed to 10% as the UK exited the lockdown period.

In the four week period, Nielsen also found that there was significant growth in the alcohol categories, with sales of beers, wines and spirits up by 31%. Frozen grew by 19% and meat fish and poultry saw a rise in sales by 15%. All of this was helped by good weather, encouraging shoppers to eat and drink outside.

Looking at the last 16 weeks, the full lockdown period in the UK, Nielsen’s data shows that shoppers in the UK spent a total of £49bn on groceries, tobacco and general merchandise. This represents an extra £3.2bn at supermarkets overall when compared to the same period last year. It also displays significant behavioural changes in consumers’ shopping habits, with visits going down and basket size going up. Moreover, the data shows that 47% of this incremental spend during the lockdown period was made at convenience stores.

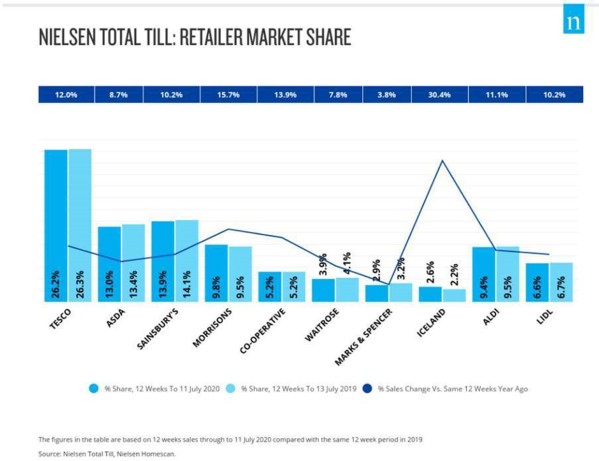

Over the last 12 weeks, Morrisons (sales growth of 15%) was the best performing of the ‘big four’ retailers. Iceland (+30.4%) and Co-op (+13.9%) also continued to perform well, as shoppers focussed on purchasing frozen food and preferred to shop at local convenience stores.

As demand for groceries returns to normal levels, Nielsen’s data shows that promotional spend is slowly increasing in recent weeks. This now accounts for 20% of all spend, up from 16% at the start of lockdown. However, this is yet to reach the same levels as the same time last year (27%).

Mike Watkins, Nielsen’s UK Head of Retailer and Business Insight, commented: “The lockdown was a period of planned, precise and predictable spend, as shoppers focussed on stocking up on the necessities – often buying more than was essential to ensure against any perceived threat of shortage or inability to go shopping. Following the reopening of pubs and restaurants on 4 July, the economy is now fully open for business and we are waiting to see how shopping behaviour will evolve.”

Watkins added: “The stalwart of the lockdown period was online grocery and there’s no signs yet that demand will slow. Shoppers also shifted a lot of their spend to convenience channels, preferring to do some of their big shop in smaller stores – possibly because of the need to remain close to home during the lockdown period.

“There are four major factors that will affect grocery shopping as we now exit lockdown. Though restaurants and pubs have reopened, we expect grocery sales to continue growing, as there remains a degree of caution when it comes to dining out. The demand for ‘staycations’ will also boost usual summer grocery levels as customers opt to stay at home or holiday in the UK. If the weather stays warm, this will be a boost for the supermarkets.

“Yet, we must be aware of the looming recession – this could place a lot of strain on consumers and where they focus their spend … retailers must be aware of the changing circumstances of customers.”

12-weekly % share of grocery market spend by retailer

and value sales % change

NAM Implications:

- Patently key for NAMs to check variance re their sales vs individual retailers to identify opportunities in these changes.

- Safe to assume online sales will continue to grow, albeit more slowly…(slightly)

- Longer-term, overall profitability of mixed business retail will be diluted as the less profitable share of business grows…

- …making it key that NAMs take a comprehensive view of the customer’s business in negotiations.