The latest data from Kantar shows take-home grocery sales rose by just 1.0% over the four weeks to 9 June, marking the slowest increase since June 2022 as poor weather and falling inflation impacted the sector. Growth in footfall also stalled, with the average shopper visiting a supermarket 16.3 times this month – down from 16.4 in June last year.

“The sixth wettest spring on record hasn’t just dampened our spirits leading into summer, its made a mark on the grocery sector too as it seems Britons are being put off from popping to the shops,” said Fraser McKevitt, head of retail and consumer insight at Kantar.

“We’re not yet reaching for those typical summertime products and are making some purchases you wouldn’t expect in June. Consumers bought nearly 25% fewer suncare items this month compared with last year, while prepared salads dipped by 11%. On the other hand, warming fresh soup sales jumped by almost 24%.”

While the drop in grocery price inflation is contributing to slower market growth, it appears to be leading to improved consumer sentiment. Kantar’s data shows the rate now stands at 2.1%, marking the sixteenth consecutive month that it has fallen. In a survey by the firm, 36% of households described their financial position as comfortable in May 2024, a proportion not surpassed since November 2021.

McKevitt commented: “The cost-of-living crisis isn’t over – far from it. 22% of households say they’re struggling, meaning that they aren’t able to cover their expenses or are just making ends meet. However, there are positive signs that many of us no longer feel the need to restrict our spending quite so much, with lower inflation helping to ease the pressure on people’s pockets. In May, we recorded the largest jump in the number of comfortable households since January 2023, rising by two percentage points on February 2024’s figure.

“Costs are falling in nearly one-third of the grocery categories we track, including toilet tissues, butter and milk. That’s a big increase from last year, when just 1% of markets were declining.”

Kantar noted that with the European Football Championship underway, supermarkets will be waiting to see if England’s and Scotland’s participation will boost trade.

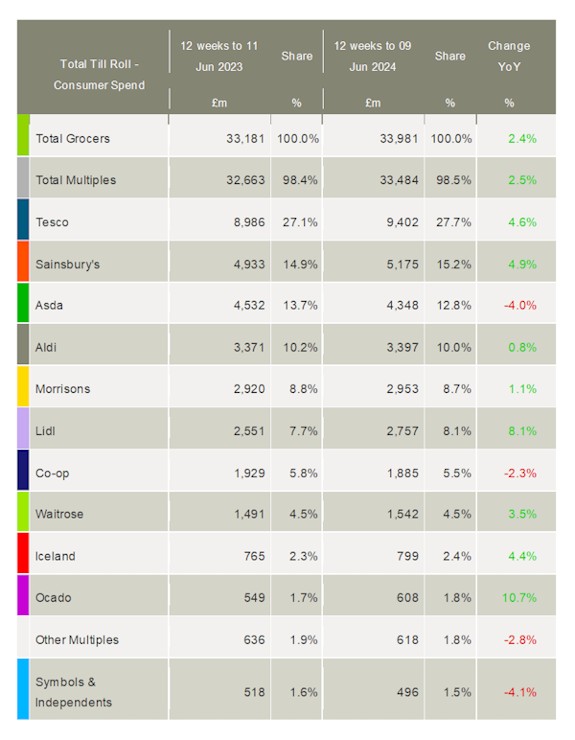

Looking at individual retailers, Ocado was the fastest-growing grocer for the fourth month in a row, increasing its sales by 10.7% over the 12 weeks to 9 June – ahead of the total online market, which saw a rise of 4.0%.

Lidl increased its market share by 0.4 percentage points to 8.1%, matching its sales growth over the period. Aldi had another disappointing month, with sales up by just 0.8% and its market share slipping to 10.0%.

Tesco achieved its highest market share since February 2022, growing 0.6 percentage points to 27.7% after a 4.6% rise in sales. Sainsbury’s saw its sales increase by 4.9%, with its share of the market increasing to 15.2%.

Meanwhile, Asda continued its poor run despite the recent roll-out of several initiatives aimed at boosting trade. Its sales fell 4.0%, with its market sliding from 13.7% to 12.8% over the year.

As Morrisons celebrates its 125th anniversary, the grocer’s sales rose by 1.1%, but its share edged down to 8.7%.

Iceland saw its sales climb 4.4%, and it now holds 2.4% of the market, up from 2.3% a year ago. This marks the first annual market share increase for the frozen-food specialist since March last year.

Waitrose welcomed 188,000 new shoppers through its doors over the 12 weeks, a greater increase than any other grocer. Its sales grew by 3.5%, with its market share holding at 4.5%.

NAM Implications:

- 21% of households still struggling with inflation…

- …although others appear to be less uncomfortable…

- …all reflected in slightly more willingness to spend.

- As a result, Tesco & Sainsbury’s appear to be matching consumer needs and are growing share at the expense of Asda and Morrisons.

- Meanwhile, discounter growth is being diluted by Aldi, resulting in a combined share with Lidl of 18.1%.

- Much now depends on Asda’s debt management for them to realise their growth ambitions…

- …and to justify any real shift in supplier strategies.