Dettol, Vim and Lifebuoy were the world’s fastest-growing brands in 2020 as shoppers protected themselves and their homes against the pandemic.

Kantar’s global Brand Footprint study, an analysis of actual shopper behaviour, found that more of the world’s top 50 brands grew in 2020 than any previous edition of the study. 29/50 of the world’s biggest FMCG brands grew the number of times they were chosen by either increasing the number of households buying them, increasing the frequency of purchase, or both, during the pandemic.

For the ninth year running, Coca-Cola remained the world’s most-chosen brand on the planet, picked 6.5 billion times globally during the year, up 4% year-on-year, based on take-home grocery sales. However, out of home sales fell 20% as most major economies experienced pandemic lockdowns, giving a different picture of their overall performance.

As online grocery shopping accelerated through the pandemic, Coca-Cola grew its e-commerce sales by 50% to be chosen 59m times online. Colgate, Lifebuoy, Maggi and Lays round out the top five most chosen brands, with Lifebuoy’s 15% growth lifting it beyond three billion times chosen and boosting it to number 3 in the ranking from 5 previously, pushing Maggi and Lay’s down a spot each.

Dettol was the fastest-growing brand of the year, with 39% growth, taking it to almost 1.4 billion times chosen and to number 16 in the Brand Footprint ranking from 27 in 2019. Its increase; more than double 2019’s growth, and four times their average growth in the past decade, was driven by an increase in penetration, with one in four households choosing Dettol during the year compared to one in five in 2019, alongside a 10% increase in purchase frequency.

Hygiene and ‘convenience’ food brands benefited most from the pandemic, Alongside Dettol’s increase in household share, Lifebuoy, Vim and Palmolive all increased their penetration rates. While in the ‘convenience’ food category Maggi, Oreo, Heinz, Lays and Barilla were all chosen by more households in 2020 vs 2019.

The growth was achieved despite shoppers reducing the number of trips to the shops as the average spend per trip increased 11%. As a result, consumers expanded their purchase choice and almost two thirds (64%) of the top 50 brands found additional shoppers during 2020.

Other key findings from Kantar’s Brand Footprint research included the proportion of growing brands that were mid-size and large increased from 50% to 54%. Meanwhile, global brands’ share of total sales fell across regions, with this dropping to 63.3% in the US (-0.4% vs 2019) while local brand share grew to 36.7%.

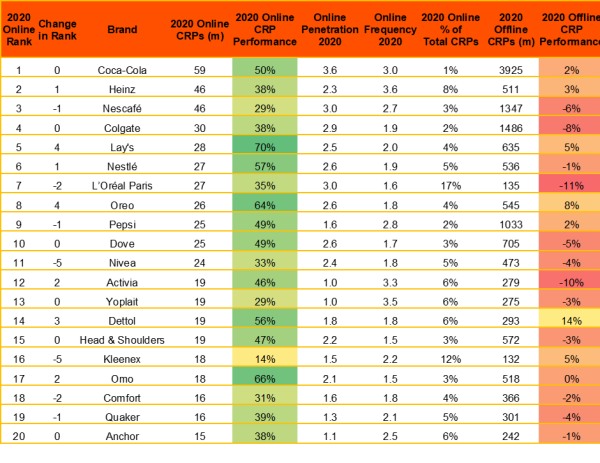

The pandemic accelerated the move to online grocery shopping, with online grocery sales increasing by over 45%. As a result, shoppers turned to the biggest brands online. The top 5 most chosen brands online were Coca-Cola, Heinz, Nescafé, Colgate and Lay’s. L’Oréal Paris was the most successful online brand with 17% of its sales happening online; its 35% online growth partially offsetting its offline decline.

A spokesperson for Kantar said: “2020 was a challenging year for companies to navigate, but FMCG brands have remained consistent and responsive to consumer trends. The events of COVID-19 turned the previously slow growth of FMCG brands on its head, leading to more of the Top 50 being in growth in 2020 than previously seen.

“With penetration being the crucial driver of brand growth, 88% of growing brands saw an increase in the number of shoppers choosing them. In 2020, five of the top 10 gains are more extensive than any seen in 2019, pointing to more consistent global growth with shopper gains seen across more markets.”

Top 25 most chosen brands globally

The Top 20 Most Chosen Online Brands

Markets included in the online ranking: Argentina, Bolivia, Brazil, Central America, Chile, Chinese Mainland, Colombia, France, GB, Greece, Indonesia, Ireland, Malaysia, Mexico, Peru, Philippines, Portugal, South Korea, Spain, Taiwan, Thailand, Vietnam

View Kantar’s Brand Footprint report here

NAM Implications:

- Data worth a detailed comparison…

- …especially re the value of heritage brands…

- …that were in the right place at the right time.

- A fact not lost on most brand owners.

- Rivals might benefit from a realistic assessment of relative competitive appeal in their categories.