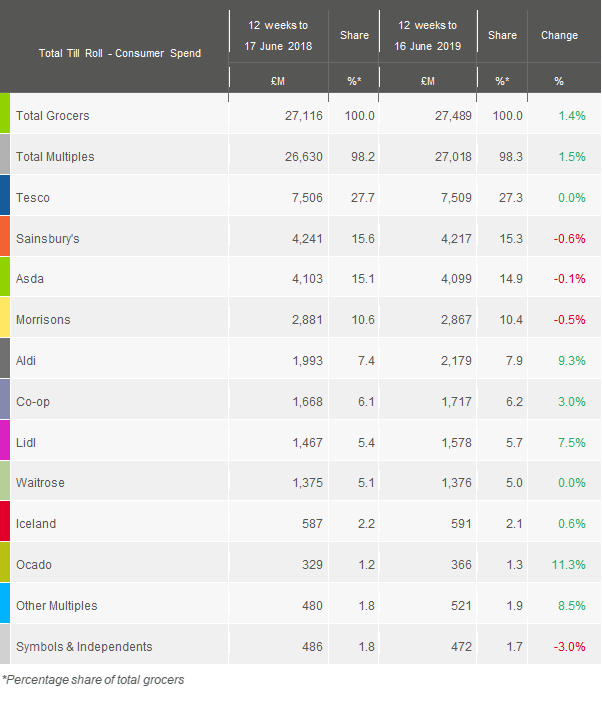

Latest grocery market share figures from Kantar show continued lacklustre performance by the Big Four supermarkets as they struggled up against tough comparatives and the strong growth of the discounters.

The total grocery sector grew a modest 1.4% year-on-year during the 12 weeks to 16 June 2019, held back by the wet start to the summer and the same period last year benefitting from a heatwave and the FIFA World Cup.

Kantar noted that these challenges were reflected in typical summer categories: in the past four weeks sales of ice cream were £15m lower than this time last year, while beer was down £17m and burgers £6m. However, shoppers did seek refuge from the cooler weather and spent more on traditional comfort foods, with fresh and tinned soup sales up by 8% and 16% respectively.

Looking at individual retailer performances, Aldi attracted an additional 883,000 shoppers through its doors during the period, with sales up 9.3%. This helped the chain to grow its market share to 7.9%, up by 0.5 percentage points on a year ago. Fraser McKevitt, head of retail and consumer insight at Kantar, commented: “Aldi’s announcement that it is rolling out more small, ‘Local’ format stores in London looks like an attempt to increase its share in the capital, where it currently takes home just one out of every £30 of supermarket spend. Grocery sales growth in London currently stands at 4% year on year, nearly three times the national rate, showing why all retailers see the capital as a major area of potential.”

Lidl, having recently announced plans for a flagship store on Tottenham Court Road in central London, also has eyes on the capital’s convenience market. However, Kantar highlighted that Lidl’s current ‘Big on the Big Shop’ advertising campaign is focused on increasing the number of large shopping trips it attracts. Nearly two-thirds of its current growth is from shoppers spending more than £25 in one go, and Lidl clearly sees value in encouraging a weekly shop. Overall, the retailer enjoyed another strong period, with sales up by 7.5%, lifting its market share to 5.7%.

Meanwhile, Tesco’s sales were flat year-on-year despite an increase in volumes sold. This was caused by the average price paid per pack falling as sales of its value own label lines like Eastman’s and Redmere Farms increased by 11%, and its ‘100 Years of Great Value’ campaign continued to offer lower prices. Tesco’s market share continued to fall, down by 0.4 percentage points to 27.3%.

Sainsbury’s saw its sales slip 0.6%, halving the rate of decline it registered last month. This was because of an increase in the number of affluent consumers visiting the retailer, with ‘AB’ shoppers increasing spend by 2% this period. McKevitt commented: “The rise in wealthier shoppers bodes well for Sainsbury’s and its plans to shake up its fresh offer, which will place more emphasis on counters, bakeries and food-to-go. The retailer will be hoping this provides another reason for shoppers to visit.”

Asda’s total sales fell by 0.1%, although its online arm enjoyed double-digit growth of 10%. The chain’s share of the overall market fell by 0.2 percentage points to 14.9%, while Morrisons’ sales decreased by 0.5%, lowering its share to 10.4%.

Waitrose’s market share slipped back by 0.1 percentage points to 5.0%, with its sales remaining flat compared to a year ago.

The Co-op continued to outperform the major supermarket chains, growing its sales by 3.0% and increasing its market share to 6.2%. McKevitt explained: “Co-op is continuing to enjoy success in London and the South, where new store openings have helped make the region its largest area of growth. The convenience retailer already boasts the highest shopper frequency in the market as customers regularly pop in for smaller baskets and this has increased even further in the latest period: the average shopper stopped by 22 times over the course of 12 weeks.”

Meanwhile, Kantar’s data showed that grocery inflation stood at 1.0% for the period with prices rising fastest in markets such as crisps, bottled cola and dog food, while falling in instant coffee, fresh bacon and detergents.

NAM Implications:

- This still seems like the discounters growing at the expense of the mults…

- And no return to former glories for the Big Four?