NielsenIQ data covering the last four weeks shows Total Till value growth in the supermarket sector increased to 5.3% from 4.7% in the previous month. Despite inflation accelerating and shoppers purchasing less, declining volumes appear to have stabilised, down 5.4% against 5.6% in the last 12 weeks, with research suggesting special offers could persuade shoppers to spend over the festive period.

Across the industry, the average spend per visit increased to £18.50 compared to £18.20 last month but is still lower than the same period last year when it was £18.70. In terms of channel performance, NielsenIQ’s data confirms that Aldi and Lidl (7.7%) are outperforming convenience stores (4.3%) and supermarkets (3.1%).

Amid the wider slowdown in discretionary spending due to inflation, general merchandise value sales in supermarkets fell 1.2%, with volumes sliding 7.6%. However, value growth across FMCG for the week ending 5 November was more robust at 5.1% at the grocery multiples and the strongest it has been since July’s record-breaking temperatures.

With the weather unseasonably warm in recent weeks, impulse categories continued to see good momentum. Crisps and Snacks (volumes +2.9%) and Soft Drinks (volumes +0.6%) were the only categories to see volume growth in the last month, with value growth of 13.3% and 9.6% respectively.

NielsenIQ expects to see growth at larger stores improve in the run-up to Christmas as savvy shoppers hunt for the lowest prices. Consumer research showed that 49% expect to find special Christmas offers from supermarkets (a direct discount on price being the most preferred) which suggests that they can be persuaded to spend provided the price is within budget. Consumers are expected to make a trade-off this year to enjoy the festive period, with Christmas expenditure cushioned by spending less eating out.

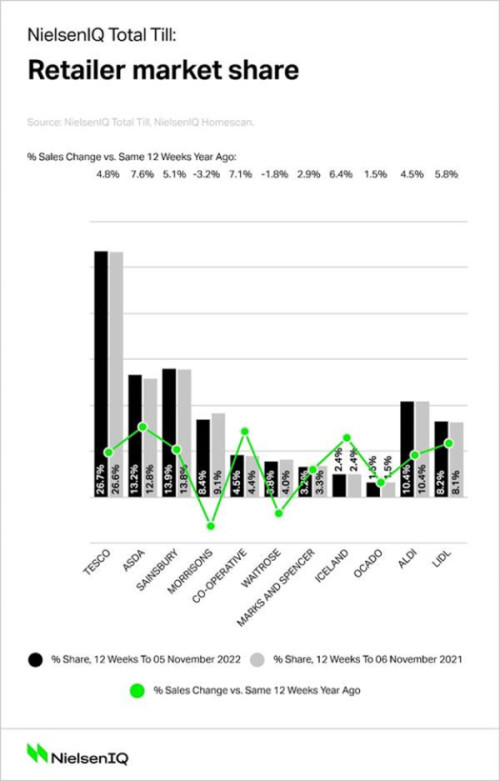

NielsenIQ found that visits to stores are up 7% compared to this time last year. Asda was the fastest growing retailer over the 12 weeks ending 5 November, with sales growing by 7.6%. Sainsbury’s was up 5.1% and Tesco grew 4.8%, while Morrisons (-3.2%) and Waitrose (-1.8%) were the only retailers to record sales declines compared to last year.

Meanwhile, the data suggests that online sales share may have reached a turning point after the recent decline slowed 1.2% compared to 7.8% over the last 12 weeks. Online share is now stable at 11.4% share of FMCG sales and increased from an 18-month low of 10.9% in October. It now compares favourably to a 12.2% share this time last year.

“There is some better news for retailers and suppliers as shoppers claim they will start to buy some items early for Christmas,” said Mike Watkins, NielsenIQ’s UK Head of Retailer and Business Insight.

“Our recent consumer survey shows that 30% of shoppers will have started their Christmas shopping this year before mid-October compared to 18% last year. 27% also say they will buy Christmas gifts when they see them in store, which suggests a ‘spreading the cost of Christmas’ mindset is ever more important this year as budgets are stretched.”

He added: “NielsenIQ is anticipating £34bn will be spent at the grocery multiples in the 12 weeks to 31.12.22, which is a growth of c4% compared to last year when there was weak post-pandemic comparatives and no real industry growth. The difference this year is that, due to inflation, we expect volumes to be down c4% with shoppers buying less and more carefully this Christmas. With the cost of grocery shopping still rising, this is motivating shoppers to shop and buy differently. With all of the big four supermarkets either giving extra price reductions or adding weekly vouchers to their loyalty schemes, this may prove the catalyst to help grow sales this Christmas.”

NAM Implications:

- Standout: Spend/visit increase: Aldi and Lidl (7.7%) are outperforming convenience stores (4.3%) and supermarkets (3.1%).

- i.e. more than double supermarkets.

- 49% of consumers expect and act on a direct discount on price.

- Online share is now stable at 11.4%

- Some pre-Christmas spending increasing at the expense of eating out.

- Still looking like a Blue, Blue Christmas…