Latest figures from Kantar show grocery price inflation declined at a slower rate this month as the proportion of items purchased on promotion dropped compared to the previous period.

The figure fell slightly to 6.8% over the four weeks to 21 January, down from 6.9% in December, marking a softer decline compared to the 2.2 percentage point decrease seen between November and December. Meanwhile, take-home grocery sales grew in value by only 2.9% over the four weeks, suggesting a further decline in volumes.

Fraser McKevitt, head of retail and consumer insight at Kantar, commented: “All eyes are back on inflation again after the Consumer Prices Index’s (CPI) unexpected jump earlier in the month. There’s been a lot of speculation about the impact the Red Sea shipping crisis might have on the cost of goods, but the story in the grocery aisles this January is more about the battle between the supermarkets to offer best value, rather than geopolitics. Retailers have taken their foot off the promotions gas slightly as we’ve come into the new year, and that’s meant inflation hasn’t fallen as quickly.”

Kantar’s data shows that items bought on offer accounted for 27% of all grocery spending in January versus 32% last month. “Christmas is always a bumper period for deals and the grocers pulled the price lever especially hard in December, as they sought to get shoppers through their doors,” said McKevitt.

“However, there’s still plenty of opportunities for consumers to make savings. The overall trend in offers is up versus this time last year, and nearly £500m more was spent on offers this January than in the same month in 2023.”

With inflation remaining stubbornly high, Kantar noted that consumers are continuing to change their behaviour to manage their costs. Research shows that people opted for more homemade meals in 2023, whilst 86 million more lunchboxes were taken out of the home to make savings.

Health was also a key factor this month, with Dry January contributing to alcohol sales falling by more than half compared to December. Almost 6% of beer packs sold this month were no or low-alcohol options, marking a rise from 4% at the end of last year. Sales of own-label plant-based ranges also increased by 8% on the month as Veganuary got underway.

McKevitt commented: “Health always comes to the fore as a priority for consumers in January, but what’s interesting this month is that we’re not seeing as big a spike in health-related categories as we have done in previous years. That’s because people are now buying more of the typical January ‘health kick’ items throughout the year. 9% of annual own-label plant-based sales were made in January in 2023, a steady decline compared with the 11% of sales in 2020.”

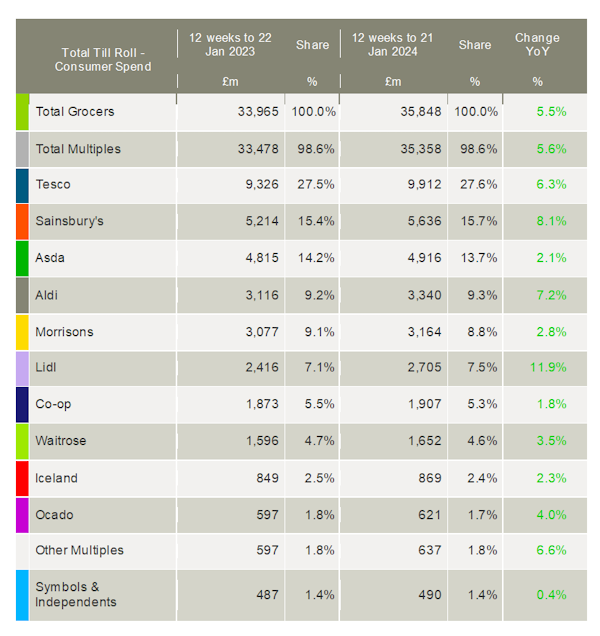

Meanwhile, both Sainsbury’s and Tesco continued their strong run, delivering market share gains over the 12 weeks to 21 January. Sainsbury’s saw its sales increase by 8.1% to take 15.7% of the market, 0.3 percentage points higher than last year, while Tesco grew by 6.3% and now has a share of 27.6%, up from 27.5%.

Lidl was the fastest-growing grocer for the fifth month in a row and the only retailer to see double-digit growth. Spending at the discounter was up by 11.9%, lifting its market share to 7.5%. Aldi also grew ahead of the market, with sales up by 7.2% and its share increasing by 0.1 percentage points to 9.3%.

It was another disappointing period for Morrisons and Asda, with their sales up by only 2.8% and 2.1% respectively, resulting in further market share losses.

Online grocery sales rose by 6.3% in the 12 weeks, ahead of Ocado’s growth, which was 4.0%.

NAM Implications:

- The standout point is Tesco and Sainsbury’s growing share at the expense Asda and Morrisons.

- (Especially critical as Asda and Morrisons are not in a position to spend their way to improved sales performance given the combination of debt burden and PE involvement)

- Aldi and Lidl are growing share but not as fast as previously…

- (probably as a result of mults price-matching?)

- The discounters vulnerability will only increase as the mults’ Retail Media Networks (RMNs) generate more incremental revenue…

- …giving the mults the option of thereby supplementing price cuts.

- Anticipate Tesco and Sainsbury’s reapplying their pressure on the promo pedal to drive further share gains.