Latest supermarket data from NielsenIQ shows an increase in total till sales (+4.7%) over the last four weeks, although there was a 6% decline in volumes compared to the 5.4% slide recorded in September. This highlights how shoppers are spending more at supermarkets due to surging inflation, but buying less.

Over the period, most categories saw value growth due to rising prices. The value increase was highest in the pet (+12.9%), dairy (+11.8%), crisps & snacks (+11.3%) and bakery (+11.2%) categories. However, sales of fresh produce fell 3.2%, and beer, wines and spirits were down 4.4%.

Volume growth was weakest in household (-9.4%), fresh produce (-8.3%), and meat, fish and poultry (-8%), as well as general merchandise (-7.1%).

NielsenIQ pointed to a survey it carried out in August, which showed British shoppers were focussing on three main coping strategies to manage rising inflation. This included monitoring the cost of their overall shopping basket (26%), opting for own-label products (27%), and shopping more at the discounters (23%). 23% are also opting to stop buying certain products.

In line with these trends, the data shows that own-label performed better than brands over the last 12 weeks, and now accounts for 53% of FMCG spend, up from 52% a year ago. Value sales of own-label grew at 6% compared to brands at 2.4%, with own-label volumes performing better in bakery (+1.9%), household (+0.5%), and dry grocery (unchanged).

Meanwhile, the trend of consumers returning to shop in-store continued with store visits up 6.5% compared with a year ago, and online visits down 9.3%. The online share of FMCG sales has now fallen to 10.9%, down from 11.1% last month.

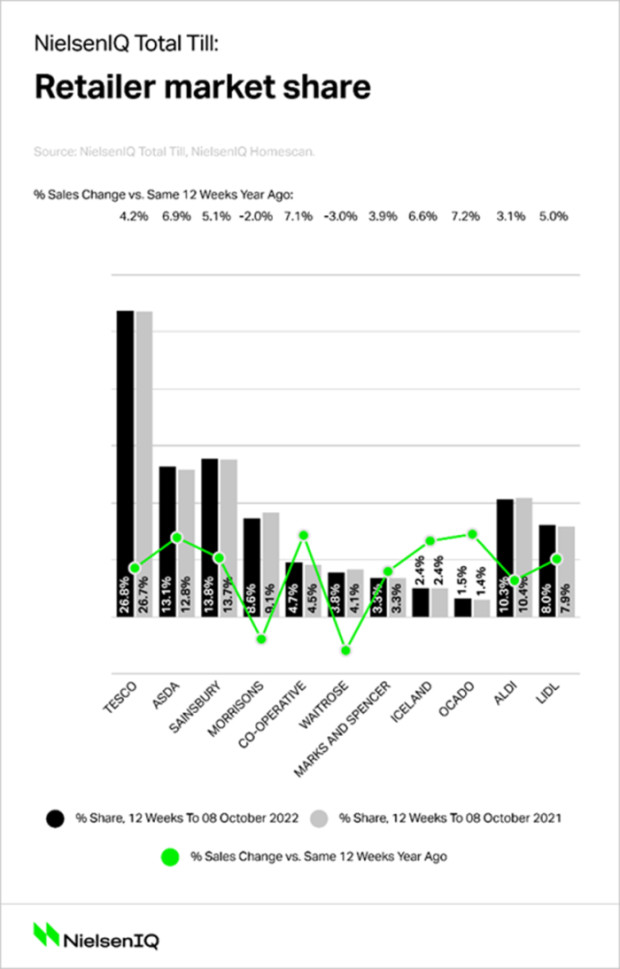

NielsenIQ’s data confirmed that Asda (+6.9%) was the fastest growing of the top three supermarkets over the 12 weeks ending 8 October, with Sainsbury’s (+5.1%) and Tesco (+4.2%) also gaining market share during this period despite the tough competition from the discounters.

Morrisons and Waitrose remained the worst performers, with sales slipping 2% and 3%, respectively.

Asda’s robust growth was partly due to it previously having weaker comparatives than the other retailers. However, with almost 9% more shoppers than this time last year, it also suggests that the retailer’s new strategies around range and value are having an impact.

Mike Watkins, NielsenIQ’s UK Head of Retailer and Business Insight, commented: “In recent weeks there has been a small shift away from fresh to frozen, slightly less spend on fruit and vegetables and fresh meat, fish and poultry and slightly more spend on impulse confectionery and soft drinks, with the latter helped by warm weather at the end of summer.

“The start of the 2022 FIFA Football World Cup should boost some categories, such as drinks and snacks, and there may be more meal occasions at home as friends and family get together to watch the sport at home. But as we edge closer to December, the challenging external economic factors that impact household budgets, such as concerns on mortgages and rising energy costs, become greater.”

He added: “It’s still very uncertain how big the all-important Christmas weeks will be based on current trends and the added pressure on shoppers who may look to opt for cheaper alternatives. But what we do know is that shoppers will be monitoring their weekly grocery spend even more closely. Some households may wish to bring forward some seasonal spending to help with budgeting, such as seasonal biscuits, chocolates and affordable gifts to spread the cost of Christmas.”