Take-home grocery sales in Ireland increased by 3.4% in the four weeks to 9 June. The data from Kantar shows that although the cooler-than-usual weather impacted barbecue category sales, it increased sales of other categories like winter warmers.

In June, there was a boost in trips to stores, up 1.5%, along with an increase in average prices of 1.3%. However, volume per trip was down 1.2% compared to the same period last year – and a change from last month’s modest rise of 0.2%.

Emer Healy, Business Development Director at Kantar, commented: “With less than typical sunny weather this June, it meant shoppers were not cracking open the barbeques or dining outdoors. As a result, they spent a combined €1.6m less on chilled salads, burgers, grills and sausages than this time last year. We did see some bank holiday weekend indulgence with sales of savoury snacks, confectionary and beer and lager up 16%,11.9% and 13.1% respectively. However, there was an increase in soup sales and home baking, which added €1m and €500k to the tills, respectively.”

Grocery inflation stood at 2.5% in the 12 weeks to 9 June 2024, down 13 percentage points versus June 2023 – the lowest inflation level since March 2022. Despite this, consumers in Ireland remain on the hunt for value in the market with over 25% of value sales on promotion.

Sales of own-label performed strongly, growing ahead of the total market at 4.9% year-on-year and holding value share of just over 48%, with shoppers spending an additional €73.5m. Premium own-label ranges continued to perform well, with shoppers spending an additional €16.8m on these lines, up 11.4% compared to this time last year. However, sales of brands were also up by 3.9% over the 12 weeks, with shoppers spending an additional €57.9m on branded lines.

Healy commented: “The great news is that Irish consumers value home-grown brands. Our latest Brand Footprint report shows that four out of the top five most chosen brands in Ireland are Irish brands, with the average Irish household buying a portfolio of 77 FMCG brands in a year – well above the global average of 66. This shows clearly how brands are still an important choice for Irish consumers”.

Meanwhile, online sales were up 16.3% year-on-year, with shoppers spending an additional €26.6m on the platform. Larger trips contributed an additional €8.9m, with more frequent trips contributing €12.4m to the channel’s growth.

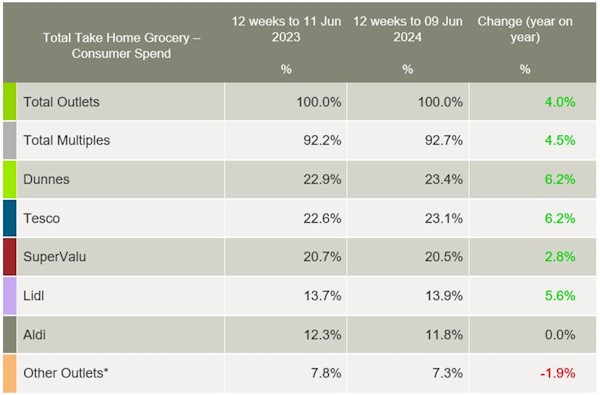

Dunnes’ market share stood at 23.4% after seeing growth of 6.2% year-on-year. Its growth stems mainly from more frequent trips but also larger trips, which contributed a combined €20.8m to its overall performance.

Tesco held 23.1% of the market, after also growing 6.2%. It saw a strong increase in trips to stores, up 7.2% year-on-year, which contributed an additional €51.1m to its overall performance.

SuperValu controlled 20.5% of the market with 2.8% growth. Its shoppers made the most trips in-store when compared to all retailers, an average of 21.6 trips, and the retailer also saw the strongest growth in volume per trip amongst all retailers, up 8.3%. SuperValu was the only retailer to attract new shoppers into its stores in the latest 12-week period, contributing a combined €66.3m additional to their overall performance.

Lidl held 13.9% share of the market with growth of 5.6%. The discounter saw the most frequent trips amongst all retailers, and this contributed an additional €38.5m to its overall performance.

Aldi’s market share slipped to 11.8%, despite more frequent trips contributing an additional €12.2m to its overall performance.