Latest data from Kantar shows that take-home sales at the leading UK grocers rose 6.5% over the four weeks to 20 April, boosted by Easter falling later this year and an uptick in promotions as stores battled for shoppers.

The figure was also lifted by rising grocery price inflation, which now stands at 3.8% – well above the recent low of 1.4% in October last year.

However, shoppers’ appetite for Easter eggs wasn’t dented, with spending up 11% compared with the season last year. Fraser McKevitt, head of retail and consumer insight at Kantar, commented: “Chocolate confectionery prices rose by 17.4% this period, the fastest of any category, but that didn’t stop the British public treating themselves this Easter. The volume of chocolate eggs sold through supermarket tills still grew by 0.4% on last year, while at the dinner table, lamb was the most popular fresh meat joint, followed by beef and pork.”

Spending on promotion reached 29.7%, its highest level this year. McKevitt said: “The grocers have been sharpening their pricing strategies to stay competitive in the fight for footfall. They’ve invested in price cuts, which were the main driver of promotional growth. Often linked to loyalty cards, spending on these deals grew by £347m. At Tesco and Sainsbury’s, nearly 20% of items sold are on a price match, and they end up in almost two-thirds of baskets.

“However, it’s not all about price perceptions alone. What’s clear is that shoppers want quality too, particularly on special occasions, and we can track that, for example, in the rapid growth of premium own label in the latest four weeks at 23.2%. Ultimately, retailers need to be seen to be offering great value, but it’s a fine tightrope to walk, particularly as they manage their own business costs.”

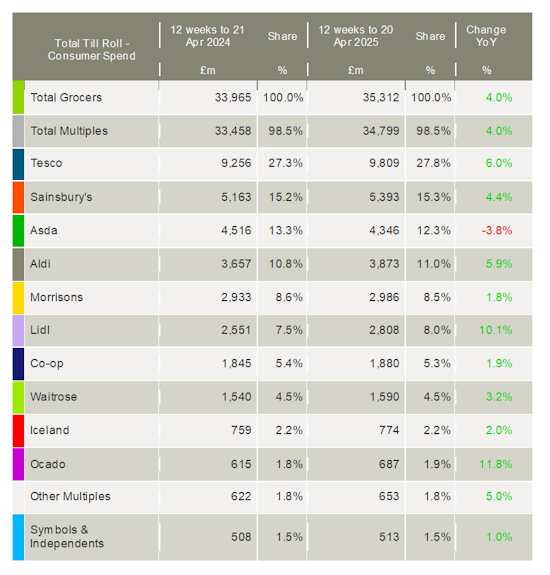

Lidl saw the fastest rise in footfall over the 12 weeks to 20 April, with shoppers walking through its doors an average of 8.8 times. This delivered sales growth of 10.1%, helping the discounter to reach an 8.0% market share. Aldi’s above-the-market sales growth of 5.9% means it now holds an 11.0% share.

Ocado was the fastest-growing retailer – a title it has held continuously for nearly a year – after its sales grew by 11.8%. Spending on groceries at M&S grew by 14.4%.

Tesco’s sales increased by 6.0%, lifting its market share to 27.8%, while sales at Sainsbury’s rose by 4.4%.

Meanwhile, there were early signs that Asda’s price rollback campaign might be having an impact on its performance. Its sales still fell by 3.8%, but this is an improvement on the declines of over 5% reported in recent months.

NAM Implications:

- Key standout has to be that Asda is the only retailer showing a fall in 12-week YOY sales…

- …indicating the scale of the challenge facing the retailer.

- A key problem is the quality of rivals by comparison…

- …along with the discounters now powering ahead amidst continuing market uncertainty.

- And a return to higher inflation, certain for further increases when additional taxes are fully reflected in the stats.

- The heavy investment in price cuts by rivals will add further pressure on Asda.

- Meanwhile, the rapid growth in premium own label poses a continuing challenge for the size of brand premia.

- Meaning consumers are less willing to accept ‘excess’ prices for brands vs their own label equivalents…