Latest data from NIQ shows total till sales growth at UK supermarkets slowed to 4.0% during the four weeks to 7th September, down from a rise of 5.5% in the previous month. The slowdown was blamed on the cooler weather and a return to regular routines for shoppers after the summer break.

The data also reveals that the online share of FMCG spend has increased to 13%, up from 12.5% a year ago. This was driven by a 1% increase in online shoppers and 6% more shopping occasions in the channel. NIQ noted that this is indicative of the evolution in how consumers shop across formats and platforms, with rapid delivery and pure players driving e-commerce growth. This is reflected in the fact that online sales grew 6.1%, outperforming bricks & mortar shopping, which increased 1.8% over the four-week period.

Overall, there was a 2.2% increase in shopping occasions across all channels as consumers aimed to take advantage of discounts, with promotional spend maintained at 25% of all FMCG sales.

Sales of general merchandise goods were down 4.5% as seasonal ranges changed and shoppers held back spend to focus instead on grocery shopping. However, there was a boost in sales for fresh food, including produce (+8.1%) and meat, fish and poultry (+5.4%). Value sales for packaged groceries (+3.9%) also grew, with unit growth of 1.8%. NIQ data recorded that the pet category was weaker, with a value sales decline of 3%, and with a change in weather, sales of soft drinks were flat (+0.1%).

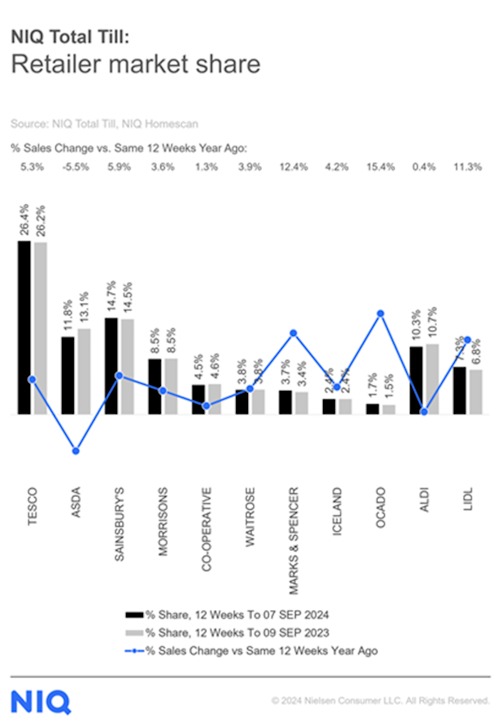

In terms of retailer performances over the last 12 weeks, Ocado (15.4%) remains the fastest-growing retailer, followed by M&S (+12.4). Morrisons continued its steady recovery (+3.6) with increased spend per visit following additional More Card offers.

Sales at Waitrose rose by 3.9% and its market share continued to stabilise after the upmarket chain attracted more shoppers and visits compared to last year following improvements in its price competitiveness. However, it was another disappointing period for Asda, with its sales sliding 5.5%.

Meanwhile, the market share of the discounters has stabilised at 17.6% and returned to the same level as in February 2023 following continued weak growth at Aldi (+0.4%).

“September is closely tied to a change in how we shop following ‘back-to-school’, so retailers typically reinvigorate marketing efforts as customers refocus on new routines as we go from Summer to Autumn,” said Mike Watkins, NIQ’s UK Head of Retailer and Business Insight.

“With some 50% of households saying they are moderately or severely impacted by the increases in the cost of living, this means retailers will need to be laser-focused in offering products and promotions that inspire customers who are budget-conscious as part of the push for sales growth in Q4.”

He added: “Many households are now budgeting for Christmas and slowly stocking their cupboards to help spread the cost. So whilst promotions are still key, assessing the impact of all media spend is more important as this helps retailers and brands get a better understanding of shopper behaviour and purchasing drivers.”

NAM Implications:

- A standout item has to be the fact that promotions on 25% of sales are driving growth, but at a cost.

- Ocado and M&S continue to shine.

- Aldi still a query as its weak growth holds back discounter share growth.

- Meanwhile, Asda awaits the arrival of a new CEO…

- The continuing market restraint:

- ‘50% of households saying they are moderately or severely impacted by the increases in the cost of living’